Assets vs. Liabilities: What They Are and How They Work

Let’s start with the basics

Assets are everything a business owns. This includes equipment, computers, office space, cash in the bank, trademarks, and more.

Liabilities are the sources of funding a business used to acquire its assets. For example, a bank loan, money invested by the owner, or loans from another company.

A key idea to remember: a company’s balance sheet must always stay in balance — total assets must equal total liabilities plus owners’ equity.

Types of Assets

Tangible Assets

Physical things a business owns — anything you can touch. Examples: vehicles, equipment, furniture, buildings, or raw materials and inventory stored in a warehouse.

Intangible Assets

Non-physical property the company owns. Examples include software licenses, patents, trademarks, and other intellectual property.

Financial Assets

Money in any form. This can include cash on hand, bank deposits, stocks, bonds, foreign currency, or notes receivable.

Types of Liabilities

Owner’s Equity

This represents the business’s own funds — the owner’s investments plus any profits the company has earned and kept instead of paying out. In other words, it’s the portion of the business financed by its owners.

Liabilities (Short-Term and Long-Term)

These are financial obligations the business owes to others. Examples include taxes payable, loans, lines of credit, customer prepayments, accounts payable to suppliers, and unpaid wages.

How Assets and Liabilities Work in Financial Statements

On a balance sheet, assets show where the company’s resources are being used, while liabilities and equity show how those resources were financed.

Liabilities can represent borrowed funds, while owner’s equity represents the company’s own funding.

Understanding the Balance Sheet

To avoid confusion between assets and liabilities, businesses track them through the balance sheet.

Non-current (Long-Term) Assets:

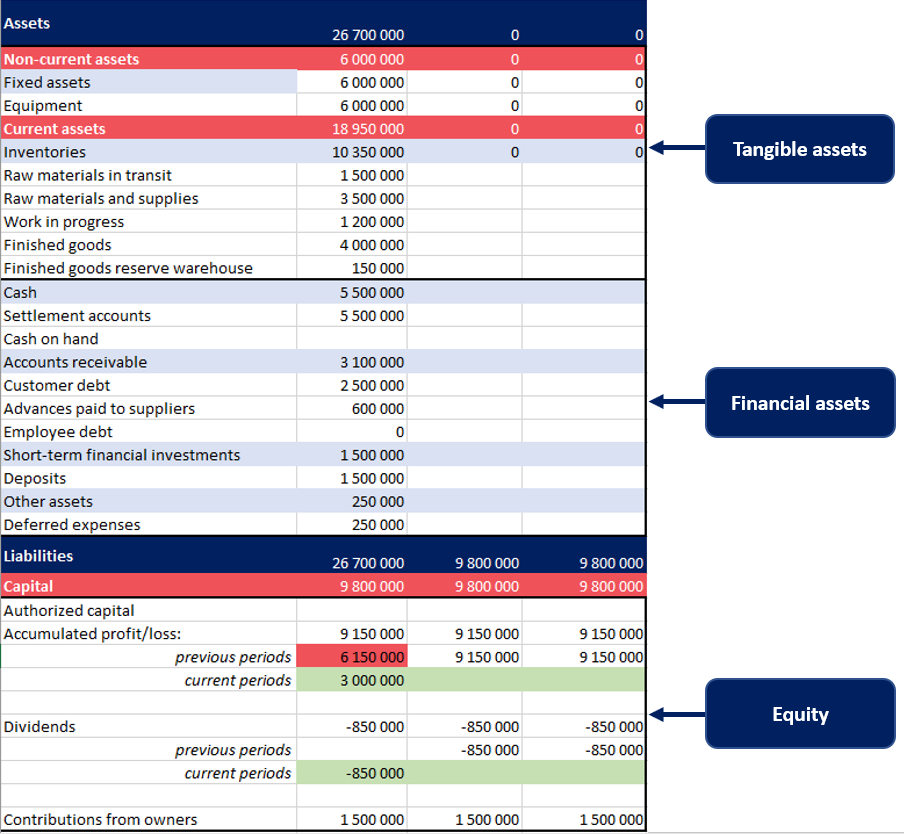

Here’s how assets and liabilities appear on the balance sheet.

Let’s start with the basics

Assets are everything a business owns. This includes equipment, computers, office space, cash in the bank, trademarks, and more.

Liabilities are the sources of funding a business used to acquire its assets. For example, a bank loan, money invested by the owner, or loans from another company.

A key idea to remember: a company’s balance sheet must always stay in balance — total assets must equal total liabilities plus owners’ equity.

Types of Assets

Tangible Assets

Physical things a business owns — anything you can touch. Examples: vehicles, equipment, furniture, buildings, or raw materials and inventory stored in a warehouse.

Intangible Assets

Non-physical property the company owns. Examples include software licenses, patents, trademarks, and other intellectual property.

Financial Assets

Money in any form. This can include cash on hand, bank deposits, stocks, bonds, foreign currency, or notes receivable.

Types of Liabilities

Owner’s Equity

This represents the business’s own funds — the owner’s investments plus any profits the company has earned and kept instead of paying out. In other words, it’s the portion of the business financed by its owners.

Liabilities (Short-Term and Long-Term)

These are financial obligations the business owes to others. Examples include taxes payable, loans, lines of credit, customer prepayments, accounts payable to suppliers, and unpaid wages.

How Assets and Liabilities Work in Financial Statements

On a balance sheet, assets show where the company’s resources are being used, while liabilities and equity show how those resources were financed.

Liabilities can represent borrowed funds, while owner’s equity represents the company’s own funding.

Understanding the Balance Sheet

To avoid confusion between assets and liabilities, businesses track them through the balance sheet.

Non-current (Long-Term) Assets:

- Resources used for more than one year — such as buildings, equipment, and software.

- Resources expected to be used, sold, or converted into cash within one year — such as inventory, accounts receivable, and cash.

Here’s how assets and liabilities appear on the balance sheet.

Reserves, Deferred Taxes, and Contingent Liabilities

In accounting, several special categories are tracked separately:

Reserves

These are funds a company sets aside to cover future expenses. Examples include reserve capital or an allowance for doubtful accounts (money the company may never collect).

Deferred Tax Assets and Liabilities

These arise from differences between financial accounting and tax accounting — usually caused by timing. They reflect taxes the company will pay or recover in future periods.

Contingent Liabilitie

These are potential obligations that might occur depending on future events. Common examples include lawsuits, product warranties, or guarantees the company has issued.

Why Understanding Assets and Liabilities Matters

Knowing how assets and liabilities work isn’t just for accountants — it’s essential for business owners too.

It helps you read financial statements correctly, understand what drives profit, and see what opportunities or risks lie within your balance sheet. These insights influence decisions about investments, borrowing, profit distribution, and even selling the business.

A common mistake among entrepreneurs is assuming profit is an asset. In reality, profit is part of equity, which sits on the liabilities side of the balance sheet because it represents a source of funding — not something the business owns.

Another misconception is that all property automatically counts as an asset. An item is considered an asset only if it’s actively used in operations and provides real economic value.

The Balance Sheet as a Management Tool

A balance sheet isn’t just a formal accounting document — it’s a strategic tool.

It shows your company’s current financial position, how your resources are structured, and how dependent you are on borrowed funds.

For LLC owners, sole proprietors, and small-business founders, regularly analyzing the balance sheet is crucial. It helps you catch early signs of imbalance between assets and liabilities and make informed decisions to keep the business healthy.

Now let's look at 18 real examples — and immediately understand whether each one is an asset or a liability.

Are Bank Accounts an Asset or a Liability?

A bank account itself isn’t an asset or a liability — it’s just a place where you keep money.

But the money inside the bank account is an asset.

On the balance sheet, this cash is usually listed simply as “cash” or “cash in bank accounts.” That’s the part that actually matters from an accounting perspective — the funds, not the account as a tool for storing them (in the table, this is the row - settlement accounts).

A bank account itself isn’t an asset or a liability — it’s just a place where you keep money.

But the money inside the bank account is an asset.

On the balance sheet, this cash is usually listed simply as “cash” or “cash in bank accounts.” That’s the part that actually matters from an accounting perspective — the funds, not the account as a tool for storing them (in the table, this is the row - settlement accounts).

Is Profit an Asset or a Liability?

Profit isn’t considered an asset.

Profit becomes part of owner’s equity, and equity is reported on the liabilities and equity side of the balance sheet because it represents a source of funding for the business.

In other words:

A company earns profit → that profit increases equity → the company can then use that equity to buy assets.

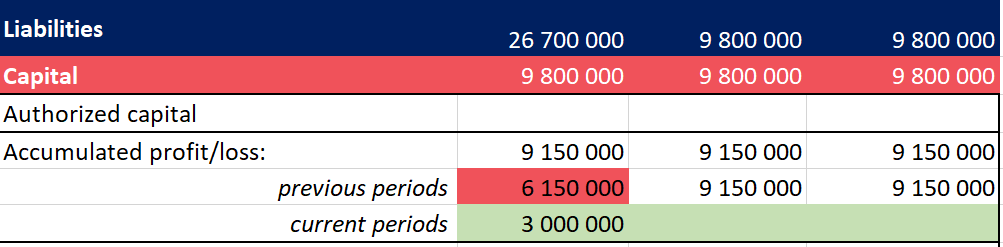

In the balance sheet, profit is shown as retained earnings, which accumulate over time — combining profits from previous years with the current period.

Profit isn’t considered an asset.

Profit becomes part of owner’s equity, and equity is reported on the liabilities and equity side of the balance sheet because it represents a source of funding for the business.

In other words:

A company earns profit → that profit increases equity → the company can then use that equity to buy assets.

In the balance sheet, profit is shown as retained earnings, which accumulate over time — combining profits from previous years with the current period.

Is Production an Asset or a Liability?

Production is considered an asset, even though the term can mean different things:

When production is complete, the result becomes finished goods, services, or work. If the product hasn’t been shipped yet, it’s recorded as inventory on the balance sheet. Once the product or service is delivered and the customer is billed, it increases cash or accounts receivable. Finally, the profit from the transaction is recorded under current period profit (equity), and the work in progress account is closed.

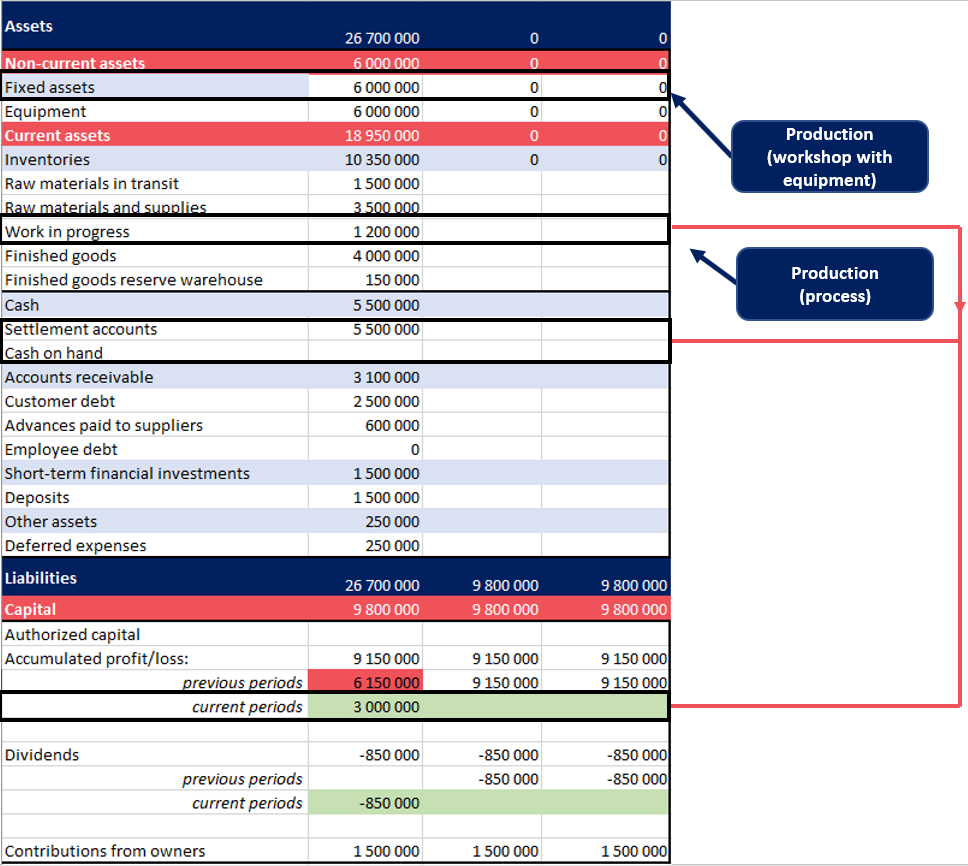

In short, production — whether as facilities, ongoing processes, or finished goods — is always treated as an asset on the balance sheet. This is what production looks like in the balance sheet

Production is considered an asset, even though the term can mean different things:

- Physical production facilities (like a factory or machinery) are long-term assets because the company has invested in them.

- The production process itself — if it will generate future profit — is also an asset. Initially, production incurs costs, which are recorded on the balance sheet as work in progress (WIP).

When production is complete, the result becomes finished goods, services, or work. If the product hasn’t been shipped yet, it’s recorded as inventory on the balance sheet. Once the product or service is delivered and the customer is billed, it increases cash or accounts receivable. Finally, the profit from the transaction is recorded under current period profit (equity), and the work in progress account is closed.

In short, production — whether as facilities, ongoing processes, or finished goods — is always treated as an asset on the balance sheet. This is what production looks like in the balance sheet

Suppliers: Asset or Liability?

Suppliers are the companies or individuals from whom your business buys goods or services. Suppliers themselves are neither an asset nor a liability — they are just counterparties.

However, transactions with suppliers are reflected in the balance sheet as follows:

Suppliers are the companies or individuals from whom your business buys goods or services. Suppliers themselves are neither an asset nor a liability — they are just counterparties.

However, transactions with suppliers are reflected in the balance sheet as follows:

- Prepaid amounts to suppliers appear as a current asset under “Prepayments”.

- Amounts owed to suppliers appear as a current liability under “Accounts Payable”.

Expenses: asset or liability?

Expenses are not reflected in the balance sheet as assets or liabilities — they are tracked in the income statement (financial results report).

The financial result of these expenses — profit or loss — is reflected in the balance sheet as part of equity under “Retained earnings.”

Expenses are not reflected in the balance sheet as assets or liabilities — they are tracked in the income statement (financial results report).

The financial result of these expenses — profit or loss — is reflected in the balance sheet as part of equity under “Retained earnings.”

Debt: Asset or Liability?

Whether a debt is an asset or a liability depends on the type of debt:

Whether a debt is an asset or a liability depends on the type of debt:

- Loans or borrowings from a bank are liabilities because the business owes money.

- The collateral or property used to secure the loan, however, is an asset.

- Employee payroll owed is a liability, since the company must pay it.

- Customer debts (Accounts Receivable) are assets, such as when the business sells goods on credit.

- Supplier debts owed to the business are assets too — for example, if the company paid a supplier in advance, that prepayment is recorded as an asset.

Fixed Assets: Asset or Liability?

Fixed assets are assets because they help a business operate and generate profit.

For example:

On the balance sheet, fixed assets typically include:

In short, fixed assets are long-term resources that the company owns and uses to run its business.

Fixed assets are assets because they help a business operate and generate profit.

For example:

- Cars in a taxi fleet

- Machines in a factory that produce parts

- Buildings used for operations

On the balance sheet, fixed assets typically include:

- Vehicles

- Equipment and machinery

- Buildings and property

In short, fixed assets are long-term resources that the company owns and uses to run its business.

Depreciation and Fixed Assets

Depreciation is not recorded as a separate item on the balance sheet.

It’s an accounting tool that shows how much a fixed asset has “worn out” over time.

Example:

In short, the balance sheet shows what the asset is still worth, while the Income Statement shows how much value was used up during the period.

Depreciation is not recorded as a separate item on the balance sheet.

It’s an accounting tool that shows how much a fixed asset has “worn out” over time.

- Depreciation is recorded in the Income Statement, not directly on the balance sheet.

- On the balance sheet, only the net (book) value of the fixed asset is shown.

Example:

- In January, a piece of equipment might be listed at $6 million.

- After one month of depreciation, its book value might decrease to $5.9 million.

In short, the balance sheet shows what the asset is still worth, while the Income Statement shows how much value was used up during the period.

Is Charter Capital (Authorized Capital) an Asset or a Liability?

Charter capital — similar to paid-in capital or owner contributions in U.S. terminology — is the money that owners invest when the business is first created. These funds are used to buy things like the first batch of inventory or equipment, and those purchases become assets on the balance sheet.

But the charter capital itself is not an asset. It represents the owners’ investment in the company, so it is recorded on the liabilities and equity side of the balance sheet under owners’ equity.

In short:

Charter capital — similar to paid-in capital or owner contributions in U.S. terminology — is the money that owners invest when the business is first created. These funds are used to buy things like the first batch of inventory or equipment, and those purchases become assets on the balance sheet.

But the charter capital itself is not an asset. It represents the owners’ investment in the company, so it is recorded on the liabilities and equity side of the balance sheet under owners’ equity.

In short:

- The money owners put in → recorded in equity (liability side)

- What the business buys with that money → recorded as assets

Customers: Asset or Liability?

Customers themselves don’t appear on the balance sheet — but the financial results of working with them do.

Here’s how it works:

Customers themselves don’t appear on the balance sheet — but the financial results of working with them do.

Here’s how it works:

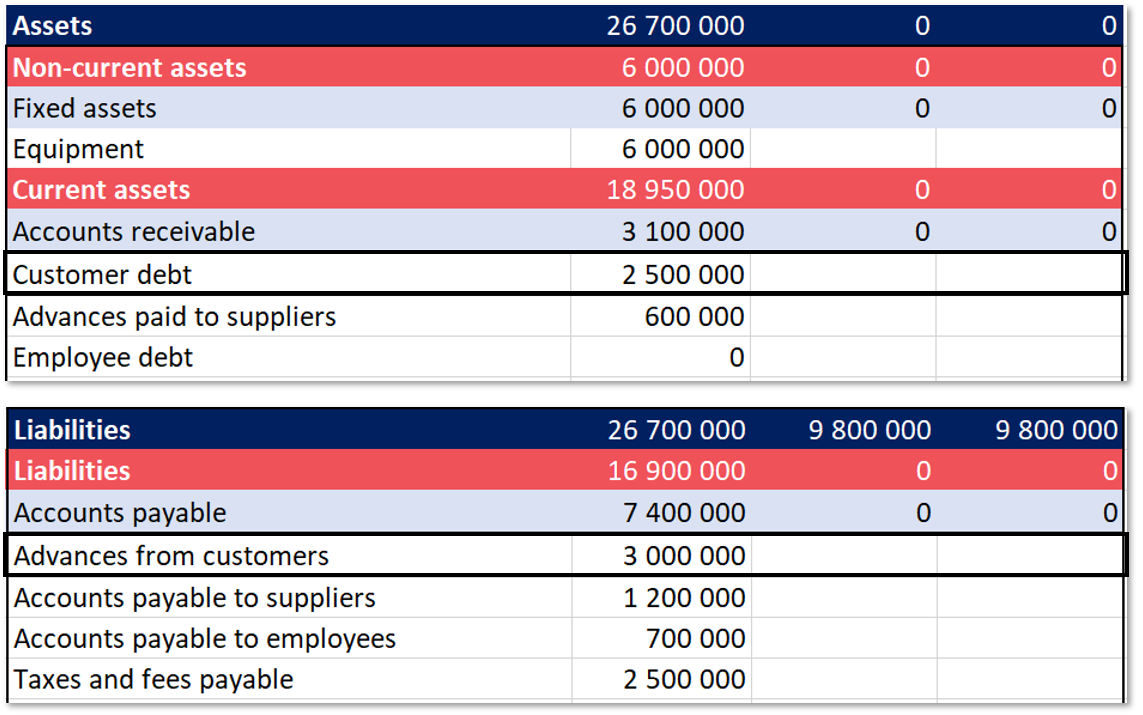

- If customers owe the business money, such as when products or services are sold on credit, that amount is recorded as Accounts Receivable, which is an asset.

- If the business owes something to customers, for example, when a customer pays in advance and the company hasn’t yet delivered the product or service, that amount is recorded as Unearned Revenue (Deferred Revenue), which is a liability.

Is Product an Asset or a Liability?

Products the business makes or sells are considered assets, because they will generate profit once sold.

On the balance sheet, products appear under Inventory, which typically includes:

In short, everything that a company stores for future sale is considered an asset under “current assets.”

Products the business makes or sells are considered assets, because they will generate profit once sold.

On the balance sheet, products appear under Inventory, which typically includes:

- Work-in-progress (WIP) — partially completed items

- Finished goods — completed products waiting to be sold

- Merchandise — items bought for resale

In short, everything that a company stores for future sale is considered an asset under “current assets.”

Intangible Assets: Asset or Liability?

Intangible assets are assets, even though they don’t have a physical form. They help the business generate future profit and are listed under Long-Term Assets on the balance sheet in the section called Intangible Assets.

This includes things like patents, copyrights, trademarks, software code, and other intellectual property.

When a Business Buys Intangible Assets?

A company can also purchase intangible assets — for example, by buying software with a one-year license. How this is recorded depends on the type of purchase:

Intangible assets are assets, even though they don’t have a physical form. They help the business generate future profit and are listed under Long-Term Assets on the balance sheet in the section called Intangible Assets.

This includes things like patents, copyrights, trademarks, software code, and other intellectual property.

When a Business Buys Intangible Assets?

A company can also purchase intangible assets — for example, by buying software with a one-year license. How this is recorded depends on the type of purchase:

- Software bought as a physical product (e.g., software on discs or hardware-based tools) is recorded as a Fixed Asset.

- Subscriptions to cloud-based software (e.g., an annual subscription to a SaaS service) are recorded in the accounts as prepaid expenses (entered in the “deferred expenses” line).

Cash: Asset or Liability?

Cash is the most liquid type of asset a business can have.

On the balance sheet, it appears under the section called Cash and Cash Equivalents, which typically includes:

In short, any money the business can use immediately is recorded as an asset.

Cash is the most liquid type of asset a business can have.

On the balance sheet, it appears under the section called Cash and Cash Equivalents, which typically includes:

- Cash in bank accounts

- Cash on hand

In short, any money the business can use immediately is recorded as an asset.

Payroll: Asset or Liability?

Payroll can appear on the balance sheet in two different ways:

Payroll can appear on the balance sheet in two different ways:

- If the business owes employees money for work they’ve already done, the amount is recorded as a liability (usually under Accrued Payroll or Wages Payable).

- If the business accidentally overpaid an employee or paid an advance, the employee now owes money back to the company. In this case, it’s recorded as an asset (often under Employee Advances or Other Receivables).

Are Revenues an Asset or a Liability?

Revenues do not appear on the balance sheet. Because of this, revenue is neither an asset nor a liability.

Revenue is recorded only in the Income Statement, where it shows how much the business earned during a specific period.

Revenues do not appear on the balance sheet. Because of this, revenue is neither an asset nor a liability.

Revenue is recorded only in the Income Statement, where it shows how much the business earned during a specific period.

Is a Bank Loan an Asset or a Liability?

A bank loan is a liability, because it represents money the business borrowed and must repay.

Depending on when the loan is due, it’s recorded as either:

Businesses often use bank loans to buy equipment or other assets — but the loan itself remains a liability on the balance sheet.

A bank loan is a liability, because it represents money the business borrowed and must repay.

Depending on when the loan is due, it’s recorded as either:

- Short-term liability (due within one year),

- Long-term liability (due in more than one year).

Businesses often use bank loans to buy equipment or other assets — but the loan itself remains a liability on the balance sheet.

Taxes: Asset or Liability?

Amounts the business owes in taxes are recorded as a liability on the balance sheet, because they represent obligations to the government.

However, if the business overpaid its taxes, the extra amount is recorded as an asset (often called a tax refund receivable or prepaid taxes). This money can either be refunded or applied toward future tax payments.

Amounts the business owes in taxes are recorded as a liability on the balance sheet, because they represent obligations to the government.

However, if the business overpaid its taxes, the extra amount is recorded as an asset (often called a tax refund receivable or prepaid taxes). This money can either be refunded or applied toward future tax payments.

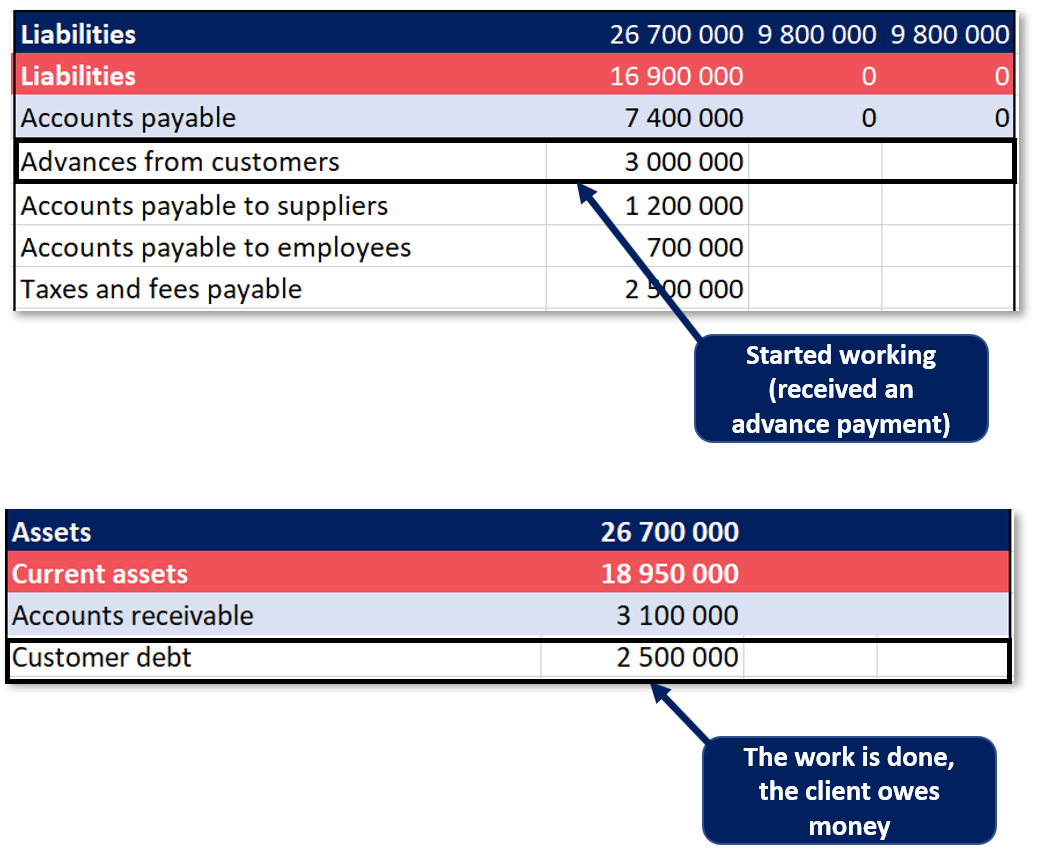

Customer Prepayments: Asset or Liability?

When a business receives money before delivering a product or service, it’s essentially holding the customer’s money until the work is completed.

Because of this, customer prepayments are a liability and appear on the balance sheet as Unearned Revenue (Deferred Revenue).

Once the business delivers the product or service in full, the obligation disappears.

If the customer still owes part of the payment (because the prepayment wasn’t 100%), the remaining amount is recorded as an asset under Accounts Receivable.

When a business receives money before delivering a product or service, it’s essentially holding the customer’s money until the work is completed.

Because of this, customer prepayments are a liability and appear on the balance sheet as Unearned Revenue (Deferred Revenue).

Once the business delivers the product or service in full, the obligation disappears.

If the customer still owes part of the payment (because the prepayment wasn’t 100%), the remaining amount is recorded as an asset under Accounts Receivable.

Prepaid Expenses / Advances Paid: Asset or Liability?

When a business pays an advance to a supplier, it is considered an asset.

For example, if the company prepays a supplier for goods to be delivered later, the amount is recorded as a current asset on the balance sheet under Prepaid Expenses or Advances Paid (part of Accounts Receivable in some reporting formats).

In short, money paid in advance represents a resource the company expects to receive in the future, so it’s an asset.

When a business pays an advance to a supplier, it is considered an asset.

For example, if the company prepays a supplier for goods to be delivered later, the amount is recorded as a current asset on the balance sheet under Prepaid Expenses or Advances Paid (part of Accounts Receivable in some reporting formats).

In short, money paid in advance represents a resource the company expects to receive in the future, so it’s an asset.